Canadian REITs can be good investments because they typically offer above-average dividend yields and give investors exposure to real estate without the difficulties of owning real estate directly (low liquidity, responsibility for maintenance, etc.).

Real Estate Income Trusts (REITs) have a unique type of corporate structure which makes theme tax-advantaged investments. They pay no corporate tax, but in return, they must meet certain criteria: they must invest primarily in real estate and pay out most of their net income as dividends.

REIT Basics

REITs are not only popular because they distribute generous dividends, but also because they’re easy to understand. Investors can picture an apartment building or an office tower and tenants paying their rent monthly. Investors are willing to purchase units of those businesses in exchange for the income and peace of mind.

The concept of being a landlord and having tenants is comparatively simple to understand. The company owns and manages real estate and receives rental income from properties such as apartment complexes, hospitals, office buildings, timber land, warehouses, hotels, and shopping malls.

Most REITs are equity REITs. They must invest most of their assets (75%) into real estate (properties) or cash equivalents. In other words, they cannot produce goods or provide services with their assets. They must generate 75% of their income from those real estate assets in the form of rent, interest on mortgages, or sales of properties. REITs must also pay a minimum of 90% percent of their taxable income as dividends to shareholders each year. Therefore, the classic earnings per share (EPS) and dividend payout ratios don’t gauge the health of an REIT.

Learn about other sectors and how to build a recession-proof portfolio. Download our free workbook now!

Types of REITs

Equity REITs

Equity REITs own and invest in property. They may own a diversified set of properties, and they generate income primarily in rent payments from leasing their properties.

Mortgage REITs

Mortgage REITs, or mREITs for short, finance property. They generate income from interest on loans they make to finance property.

Hybrid REITs

Hybrid REITs do a bit of both, as they own property and finance property.

In general, REITs offer great investment opportunities by their nature. A growing economy leads to growing needs for properties. REITs can grow organically as the population requires more industrial facilities, healthcare centers, offices, and apartments.

Sub-Sector (Industry)

| REIT – Diversified | REIT – Mortgage | REIT – Specialty |

| REIT – Healthcare Facilities | REIT – Office | Real Estate – Development |

| REIT – Hotel & Motel | REIT – Residential | Real Estate – Diversified |

| REIT – Industrial | REIT – Retail | Real Estate Services |

REITs strengths

REITs are unique as they distribute most of their income. In fact, they exist to pay generous distributions. This makes them one of the retirees’ favorite sectors! Since these businesses must give most of their profits to shareholders, it’s easy to understand how most of them offer a relatively high dividend income. This is one of the rare sectors where you can find “relatively safe” stocks paying 5%, 6% even 7%+. Investors must be careful not to get too greedy, though. We have seen several REITs cutting their dividends due to poor management or economic downturns.

REITs usually bring stability in a portfolio along with higher yield. It’s a great sector to start with if you’re looking for additional income. Real estate brings great diversification to your portfolio. Research has proved that REITs are not directly correlated to stock market movements over the longer term.

Finally, since most of them operate with escalator contracts, they offer great protection against inflation. Many income trusts include yearly rent increases in their leases to ensure rental income matches inflation. Some REITs also use Triple-Net leases, where the tenants is responsible for insurance, taxes, and maintenance costs, thus reducing the REITs’ expenses (and risk of unexpected charges!).

Learn the strengths and weaknesses of other sectors and how to build a recession-proof portfolio. Download our free workbook now!

REITs weaknesses

One of the REIT sectors’ favorite ways to finance their new projects is to issue more units. Therefore, if a company purchases a property generating $20M per year but needs to issue more units to finance the purchase, you must look at the net outcome for unitholders. If the FFO per share drops, this is not necessarily good for you as it will affect the REIT’s ability to increase its dividend in the future.

Another downside related to their business model is their lack of flexibility. We have seen many times where REITs try to shift their focus from one industry to another. In most cases (H&R, RioCan, Boardwalk and Cominar to name a few), the change of trajectory comes with a dividend cut and a loss in value for unit holders. A REIT wishing to get rid of their shopping malls to buy more industrial properties will likely have to sell properties at a lower price and pay a hefty one to buy more appealing assets.

Finally, don’t make the mistake of thinking REITs are safer than other sectors. They are companies facing challenges while benefiting from tailwinds. While you may argue that an apartment building can’t go anywhere, I would answer back that if you have one hundred empty apartments due to an oversupply in a neighborhood, your money will also go nowhere.

The REIT sector is best for income investors.

Target sector weight: For income-seeking investors, you can aim at 15% to 30% (if you invest in various industries). For growth investors, REITs could represent a 5%-15% portion of your portfolio.

How to get the best of REITs

While REITs are part of a short list of sectors that are perfect for retirees or other income seeking investors, it is important to understand that they cannot be analyzed using the same metrics as other sectors.

Funds From Operations (FFO/AFFO)

The Funds from Operations (FFO) and Adjusted Funds from Operations (AFFO) are probably the most useful tools to analyze a REIT’s financial performance. Those two metrics replace the earnings and adjusted earnings for a regular stock. While those are different metrics, it’s all about cash flow and the REITs’ ability to sustain their dividend payments. Fortunately, we can find those metrics inside each REIT’s quarterly report and subsequent press release. It’s important to follow not only the total FFO/AFFO, but also the FFO/AFFO per share (or unit of ownership) rather than earning per share (EPS) or adjusted earnings per share.

FFO = Earnings + Depreciation (Amortization) – Proceeds from Property Sales

AFFO = Earnings + Depreciation (Amortization) – Proceeds from Property Sales – Capital Expenditures

Loan to Value Ratio (LTV)

The loan to value ratio (LTV) is a great tool to analyze the REIT’s future ability to raise low-cost capital. The LTV is easy to calculate from the financial statement, as you only need 2 measures of data:

LTV = Mortgage Amount / FMV of properties

You certainly don’t want to invest in a REIT showing a high LTV. This means that their credit rating may be at risk and the price for future debt will be higher. In other words, it could mean less money for future dividends.

Net Asset Value (NAV)

The last metric to follow for REITs is the Net Asset Value (NAV). The NAV (usually shown by units) can be translated to the equivalent of a Price to Book ratio.

NAV = Total Property Fair Market Value – Liabilities

The idea is to compare a few REITs from your list against one another. This is how you should be able to find the ones with the best metrics. A lower than industry NAV is either a riskier play or a value play. The AFFO and LTV will tell you which one it is.

Don’t use the payout ratio to assess REITs’ dividend safety

Trusts have a special tax structure and they are required to distribute 90% of their taxable income. Therefore, using the payout ratio (which is based on earnings) doesn’t help. The metrics you’re looking for is the Funds From Operations (FFO) and the Adjusted Funds From Operations (AFFO) payout ratios.

Funds from Operations Payout Ratio

Formula: DIVIDEND PER SHARE (DPS) / (ADJUSTED) FUNDS FROM OPERATIONS (FFO) PER SHARE

Since REITs are required to distribute at least 90% of their net earnings, adjusted funds from operations (AFFO or FFO) is a more precise metric. Like the payout and cash payout ratio, it’s always preferable to look at a long-term trend of the metrics over several years.

Pros: Similar to the cash payout ratio, you get a clear picture of how much cash the company has to pay dividends.

Cons: In most cases, you can’t calculate the FFO payout ratio yourself or find it in general finance websites (therefore we try to mention it in our DSR Stock cards). You must rely on the company’s information found in their quarterly earnings reports. It requires additional time to establish a trend over several years.

REITs valuation

Valuing a REIT is like valuing any stock. Since REITs distribute most of their profits as dividends, I generally use the Dividend Discount Model (DDM) to value them. However, some of other REIT-specific metrics we’ve seen are also vary valuable when valuing REITs.

Net Asset Value (NAV) is another estimate of intrinsic value. It’s the estimated market value of the portfolio of properties. One way to evaluate this value is to divide the current net income from the properties by a capitalization rate that’s fair for those types of properties. NAV can potentially understate the value of the properties because it might not capture value appreciation of properties during strong growth periods in the market. Compare the NAV to the price of the REIT.

We’ve seen that Funds from Operations (FFO) are far more important than net income for a REIT. Due to the tax structure of REITs, earnings mean almost nothing; instead, it’s all about cash flow. When calculating net income, depreciation is subtracted from revenues; depreciation is a non-cash item and might not represent a true change in the value of the company’s assets. FFO adds depreciation back to net income, providing a better idea of the cash income for a REIT.

Adjusted Funds from Operation (AFFO) is arguably the most accurate metric of income measurement of all for REITs. AFFO takes FFO but then subtracts recurring capital expenditures on maintenance and improvements. It’s a non-GAAP measure, but a very good gauge of the actual profitability and amount of cash flow available to pay out in dividends.

Overall, it’s good to look for REITs that have diversified properties, strong FFO and AFFO, and a good history of consistent dividend growth.

REIT advantages and disadvantages

Before presenting some of our picks for Canadian REITs, let’s sum up the advantages and disadvantages of REITs.

Advantages:

- Usually have above-average dividend yields.

- Are good protectors from inflation. If inflation occurs, property values and rents increase over time, but fixed-interest on the debt that finance the properties doesn’t.

- Real estate, if managed conservatively, can be a reliable investment for income and in times of recession, assuming tenants pay their rent.

Disadvantages:

- Often have lower dividend growth than companies in other sectors.

- Generally use debt to add to their property portfolio, but their larger debt loads is used for conservative, appreciating assets.

- Since they have to pay most of their income as dividends, they have little downside protection from recessions. They might have to trim the dividend if their cash flow dips below their distribution levels. There are, however, some REITs that have good track records of consistent dividend growth, despite market downturns.

Favorite Picks

Based on a mix of diversification, growth perspective, and dividend growth, we have identified three Canadian REITs that we like:

Granite (GRT.UN.TO)

GRT used to be an extension of Magna International (MG.TO). In 2011, Magna represented about 98% of its revenues. It is now down to 25% as of November 2023 (with Amazon as its second-largest tenant with 4% of revenue). You’ll notice that each year, GRT reduces its exposure by a few percentage points. Management has transformed this industrial REIT into a well-diversified business without adversely affecting shareholders. GRT now manages 138 properties across 7 countries. Each time we review this stock card, the number of properties increases while the exposure to Magna Intl reduces. The REIT also boasts an investment grade rating of BBB/BAA2 stable. With a low FFO payout ratio (around 70-75%), shareholders can enjoy a 5% yield that should grow and match or beat the inflation rate. This is among the rare REITs exhibiting AFFO per unit growth while issuing more units to finance growth.

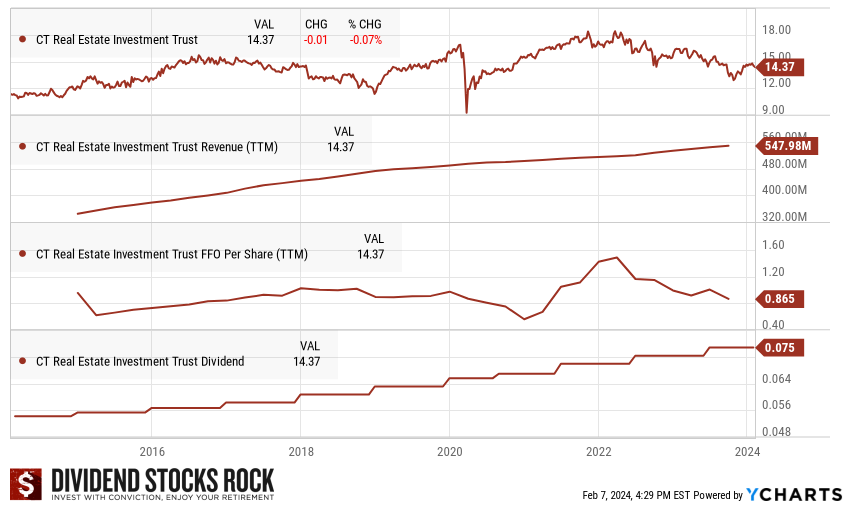

CT REIT (CRT.UN.TO)

An investment in CT REIT is primarily an investment in Canadian Tire’s real estate business. If you think this Canadian retail giant will do well in the future, but you are more interested in dividends than pure growth, CT REIT could be a good fit for you. Canadian Tire has exciting growth plans that will eventually lead to more triple-net leases for CT REIT. The fact that CRT pays a monthly dividend with a 6% yield is highly attractive to income-seeking investors. On top of that, CT REIT exhibits a decent dividend growth rate policy, matching and beating inflation over the long haul. In the past 10 years, the company grew its revenue and AFFO by mid-single digits numbers. This makes it a perfect candidate for an income-focused portfolio. Canadian Tire has done well in the past 5 years thus far and has proven the resilience of its business model. It’s a sleep well at night REIT that should please all income-seeking investors.

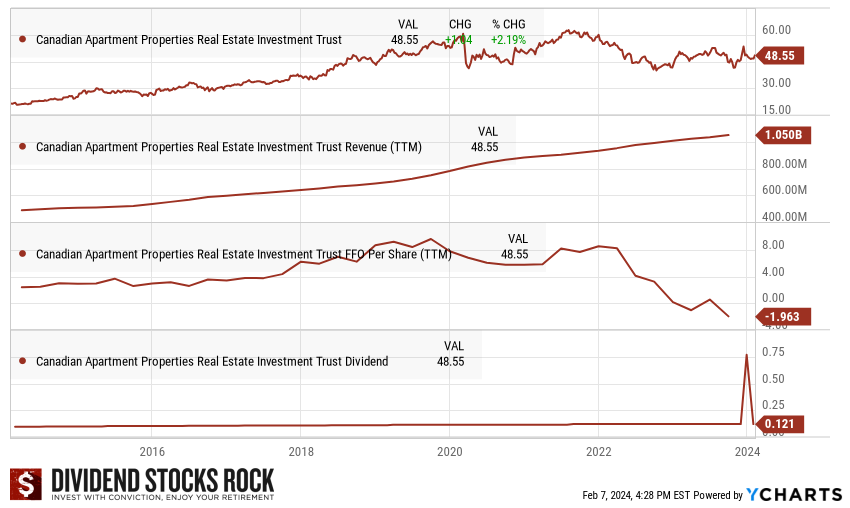

Canadian Apartment Properties (CAR.UN.TO)

If an investor is looking for a steady source of income that will keep up with inflation, CAPREIT should be on their watchlist. In addition to enjoying a strong core business in Canada, CAPREIT is expanding its business in Ireland and the Netherlands. This gives them additional geographic diversification. CAPREIT continues to exhibit high-single-digit organic growth while raising additional funds to acquire more buildings. Unfortunately, the REIT neglected to increase its dividend in 2020. We cannot blame management for being overly cautious over the pandemic; they were fortunately stronger in 2021 and won back their dividend safety score of 3.

Those REITs are great, but there’s more!

If you look at past performances, Real Estate Income Trust is one of the best performing classes during high inflation periods since the 70s. Unfortunately, not all REITs are created equal and you must do adequate research to be sure to buy the right ones.

Watch this webinar during which I answer questions like:

- How about REITs paying a 10% yield

- How to make sure the REIT’s distribution is safe

- Which metrics to consider during my analysis?

- Should I consider mortgage REITs?